The economic problem

The fundamental economic problem arises from unlimited wants and needs and limited scarce resources, to fulfil these needs and wants.

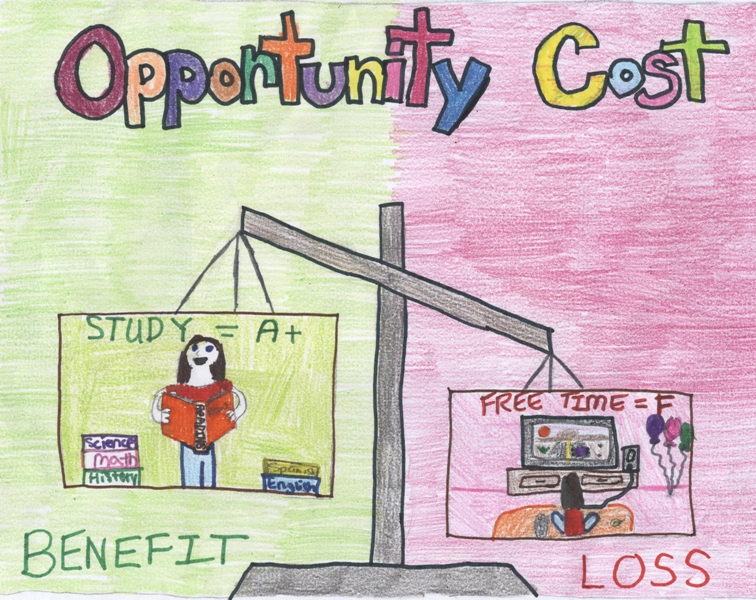

Opportunity cost

This leads on from the problem of scarcity. Opportunity cost is the cost of forgoing the next best alternative. In a situation which a choice needs to be made between several mutually exclusive alternatives given limited resources. Assuming the best choice is made, it is the 'cost' incurred by not enjoying the benefit that would be had by taking the second best choice available.

The production possibility frontier and the problem of scarcity.

The PPF shows the various combinations of goods and services that can be produced, assuming that inputs into the production process are fully utilised, with no spare capacity.

So what this diagram is showing at point A 15 units of goods are demanded and 22 services. However if the population require more services then the economy would produce 11 units of goods and increase services to 25.

At point A&B scarcity occurs. For any point inside the frontier, such as C, there is idle resources so this means that production can increase without diverting resources away from another use.

At point C, THERE IS NO OPPORTUNITY COST.

The PPF shows the various combinations of goods and services that can be produced, assuming that inputs into the production process are fully utilised, with no spare capacity.

So what this diagram is showing at point A 15 units of goods are demanded and 22 services. However if the population require more services then the economy would produce 11 units of goods and increase services to 25.

At point A&B scarcity occurs. For any point inside the frontier, such as C, there is idle resources so this means that production can increase without diverting resources away from another use.

At point C, THERE IS NO OPPORTUNITY COST.